January 2024

Don't lose your head.

This post marks the beginning of a series of monthly market updates. What better way to start 2024 than by reflecting on 2023 and “taking the temperature” of the S&P 500?

Year in Review

US equity markets had a stellar year in 2023. The Nasdaq was up 43%, the S&P 500 up 24%, and the Dow Jones Industrial Average up 14%. Some tailwinds may have contributed to this success. Volatility decreased by 43%, the dollar index is down 2%, and oil down 11%. Popular alternative assets also performed well. Gold was up 13%, and Bitcoin saw a whopping 156% increase. Others remained noticeably flat with the TLT gaining only 3%, and silver not moving by even a percent. Popular stocks like Apple (up 49%) and Tesla (up 102%) have either broken new highs or regained much of the ground lost in 2022.

It seems that many market participants are now satisfied, perhaps even a little complacent. What has changed so drastically between last December and today? Was it the fundamentals? Was it the macroeconomic outlook? Was it advances in artificial intelligence? Or was it simply people’s expectations?

I believe it is a shift in mindset, not so much the big picture.

NOPE

I remember the end of 2022 very clearly. I had just started taking habitual notes on finance podcasts to better understand markets. Seeing George Noble hosting spaces on Twitter, I tuned in and felt clever because I could connect the dots between him and Peter Lynch after just having read One Up on Wall Street. If only I knew at the time that feeling clever is a red flag.

The market’s atmosphere was one of pessimism. Suggestions that the market would do better than expected in 2023 were received with skepticism at least and ridicule at worst. I thought to myself, “All of these people are bearish, and they sound smart too. Who am I to think otherwise?” This was before I saw herd psychology in action.

When January 2023 came around, the market immediately made a fool of the crowded bears. The Nasdaq ripped 11%, and George Noble’s NOPE ETF lost 57% of its value in that month alone. I was stunned. How could this happen? He sounded so smart, and he was an industry veteran. Surely someone like that would be a savvy investor with other people’s money, right? I would come to realize that anyone can fall victim to motivated reasoning, even someone like George Noble.

My intention is not to pick on Mr. Noble but rather to provide a cautionary tale of what can happen due to rigid thinking and hot emotions. Truly savvy traders and investors are wed to their process, not to some narrative or how they happen to feel at the time.

The bears of late 2022 turned out to be wrong, but what does it mean when most of them have given up by late 2023? Are we really in the clear?

Benjamin Graham is Dead

I like to think of myself as a logical person, so I wish dearly that fundamental investing is taken seriously. I simply do not see it in this market.

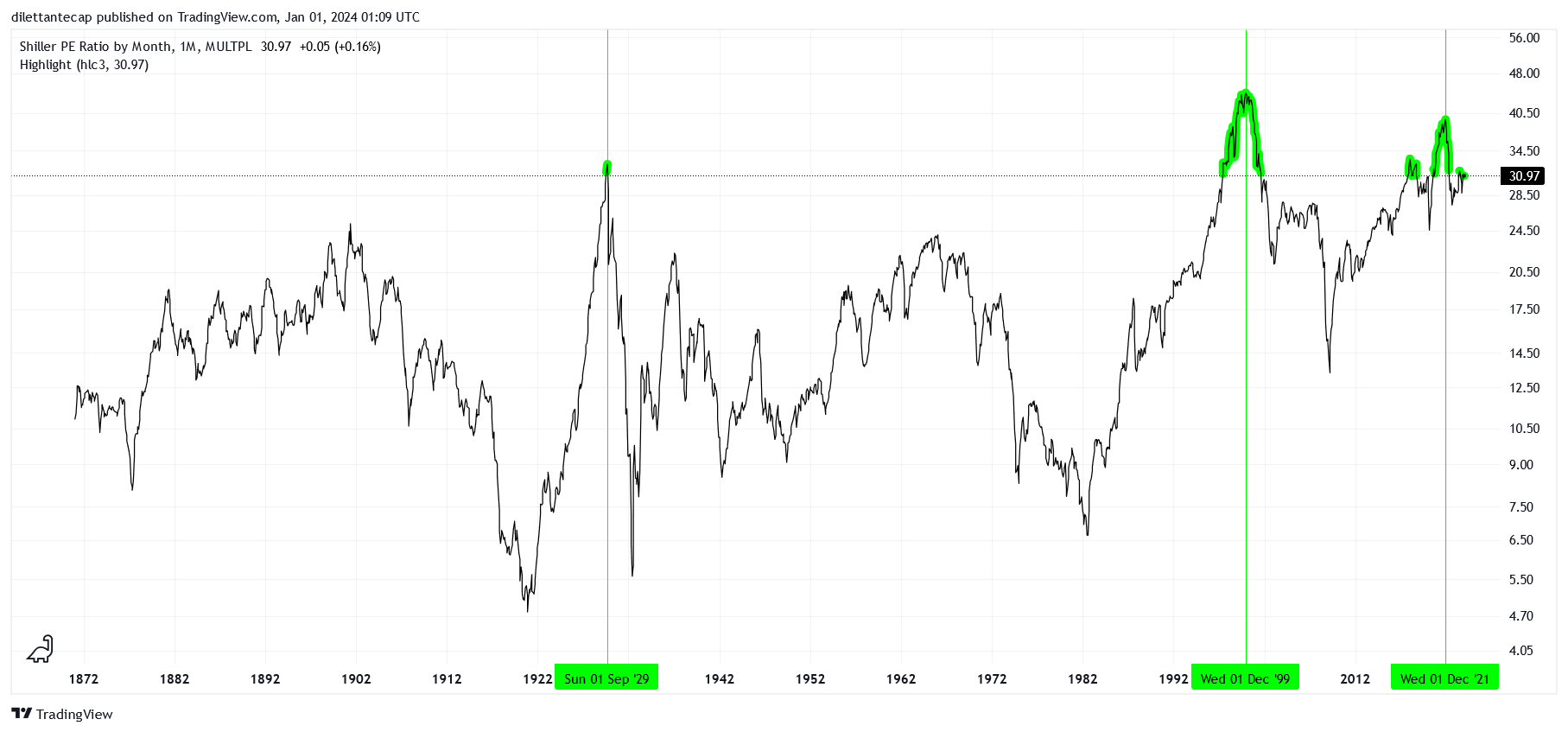

The Shiller P/E ratio of the S&P 500 currently sits very close to 31, where it has been since 2017 (with minor deviations). Just to elucidate how expensive this is, we are near the 95th percentile going back to 1871. The two other periods of time with such elevated valuations were 1929 and 1997-2002. You have probably heard of the Great Depression and the Dotcom bubble. These were not good investment opportunities, to say the least.

If we price the S&P 500 cash index relative to corporate profits after tax, we are in the 77th percentile going back to 1947. Relative to gold since 1884, the 87th percentile. Relative to M2 money stock since 1959, the 94th percentile. Relative to GDP since 1947, the 98th percentile. While these metrics tell slightly different stories, none of them indicate that this market is cheap.

Be Careful

I hope that I do not come across as overly pessimistic. Bears are never fun at parties, after all. I think that this market has enough momentum to push a little higher, but otherwise, it doesn’t seem like a safe long-term investment given historical precedent.

What I would like to highlight is that if you are looking to invest in 2024, ask yourself if it must be in U.S. equity markets. There is a whole world of stock markets (literally) and alternative asset classes beyond equities. Are you sure that buying Apple at 31 times earnings and nearly 8 times revenue is the best investment opportunity that you can find?

I challenge you to find something better.